Duplicate charges can be frustrating, especially when the same purchase appears more than once on your bank account, credit card statement, or payment history. Whether the issue is caused by a merchant error, a technical glitch, a subscription renewal problem, or an accidental double payment, it can leave consumers wondering whether they have been overcharged and how to recover their money.

The good news is that most duplicate charges and double billing issues can be resolved successfully when addressed promptly. Understanding why duplicate charges occur, how to verify the transaction, and when to contact the merchant or your bank can help you take the right steps toward a faster resolution and avoid unnecessary financial stress.

What Are Duplicate Charges?

A duplicate charge occurs when your bank account, debit card, or credit card is billed more than once for the same transaction. This is also called double billing or a duplicate transaction. The result is that you pay more than you should for a single purchase, product, or service.

Common types of duplicate billing errors include:

- Credit card duplicate charge: The same purchase appears twice on your credit card statement.

- Bank account double debit: Your checking account is debited twice for one transaction.

- Subscription double billing: A membership service charges you twice in the same billing cycle.

- Merchant processing mistake: A cashier accidentally runs a card twice at a point-of-sale terminal.

- Incorrect charge: A billing amount that does not match the agreed price or invoice.

Duplicate charges are distinct from unauthorized charges, which occur when someone uses your payment information without permission. Both are billing errors, but they have slightly different dispute processes.

Common Causes of Duplicate Charges

Understanding why duplicate charges happen can help you identify them faster and prevent them in the future. Here are the most frequent causes:

- Payment terminal errors: A slow or malfunctioning card reader may process a transaction twice if the cashier or customer taps or swipes the card more than once.

- Merchant processing issues: Software bugs in a retailer's payment system can send duplicate authorization requests to your bank.

- Subscription renewals: Auto-renewing memberships (streaming services, software subscriptions, gyms) sometimes generate double payments due to billing system glitches.

- Technical glitches: Network timeouts during checkout can cause a transaction to be submitted multiple times.

- Delayed transaction posting: Some transactions appear as pending for several days. Consumers who see a pending charge and pay again manually create an accidental double payment.

- Human error: Billing staff entering manual invoices or processing refunds incorrectly can introduce duplicate entries.

- Payment processor errors: Third-party payment processors like Stripe, Square, or PayPal occasionally generate duplicate charges during system updates or downtime.

How to Tell Whether a Charge Is Truly a Duplicate

Not every charge that looks like a duplicate actually is one. Before you dispute anything, take a moment to verify what you are seeing.

Pending Authorizations

When you make a purchase, your bank first places a temporary hold on the funds — this is an authorization. The actual charge posts later. For a brief period, you may see both a pending authorization and a posted charge. This is normal. Wait 2 to 3 business days to see if one of them disappears before filing a dispute.

Separate Legitimate Transactions

If you bought two items from the same merchant on different days, both may appear as separate charges. Check the transaction dates carefully. If the dates and amounts are identical, it is likely a duplicate charge.

Temporary Holds

Hotels, car rental companies, and gas stations frequently place temporary holds on your card that exceed the final purchase amount. These holds typically fall off within a few days and are not billing errors.

How to Verify a Duplicate

To confirm you are dealing with a genuine duplicate charge:

- Compare transaction dates — are both charges on the exact same date?

- Compare transaction amounts — do both show the same dollar amount?

- Check merchant names — do both entries show the same merchant?

- Cross-reference with your receipts — does your receipt show only one transaction?

If all three match, you most likely have a duplicate charge on your hands.

What to Do Immediately After Finding Duplicate Charges

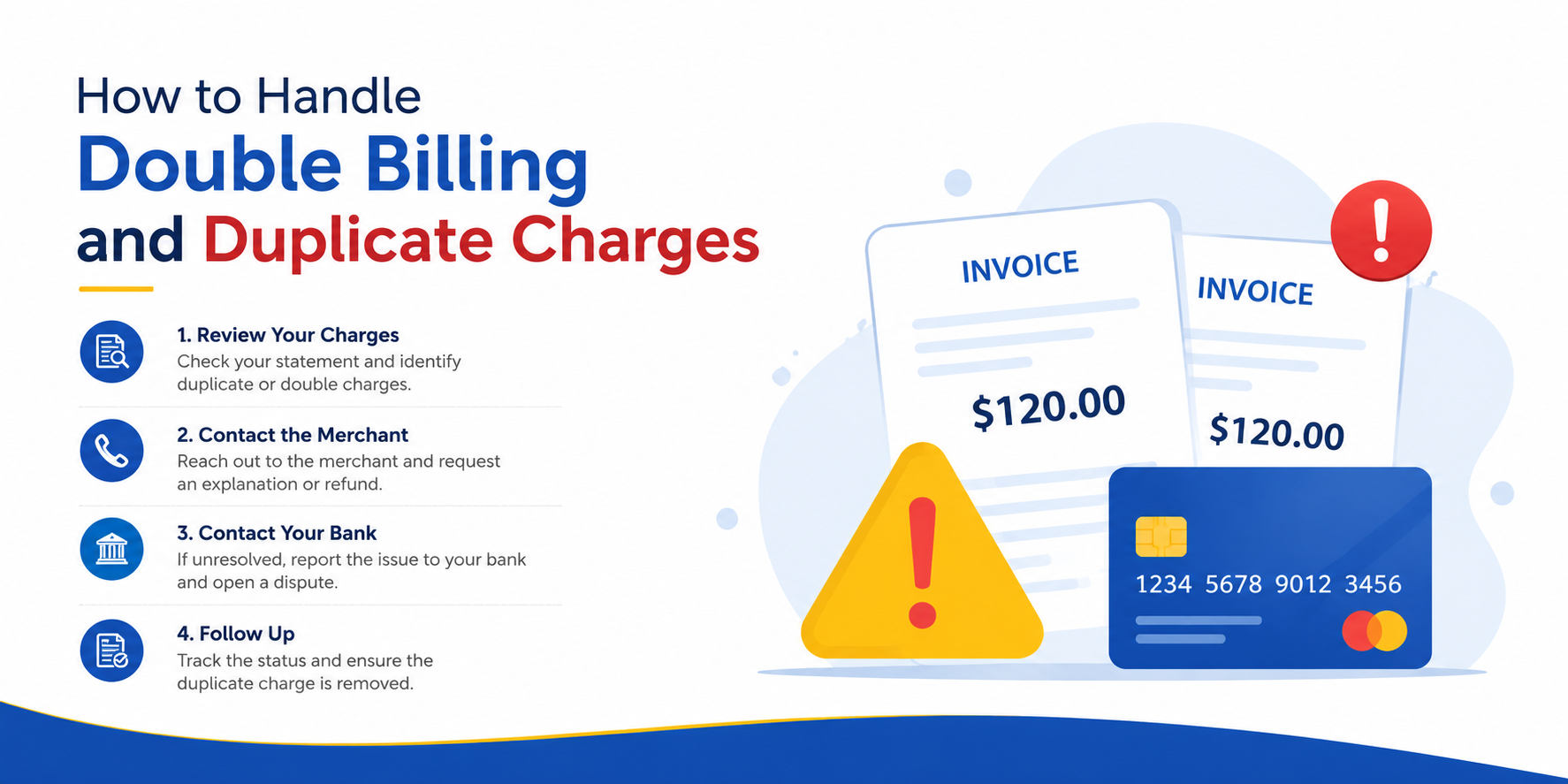

Step 1: Review Your Account Carefully

Log into your bank or credit card account online and examine the transaction history. Look at transaction dates, merchant names, and exact dollar amounts. Take screenshots of both charges for your records. Note the reference numbers if visible.

Step 2: Gather Documentation

Before contacting anyone, collect your evidence. This will make every subsequent step faster and more effective. Gather:

- Original receipt or order confirmation email

- Bank or credit card statement screenshots

- Any email or text confirmation from the merchant

- Photos of the transaction details on your device

Step 3: Contact the Merchant

Call or email the merchant's customer service or billing department. Be direct: explain that you have been charged twice for the same transaction, provide the date and amount, and request a refund for the duplicate charge. Most reputable businesses will resolve this quickly.

Step 4: Monitor Your Account

Some duplicate charges reverse automatically within 3 to 5 business days — particularly pending authorizations. Continue monitoring your account while you wait for a response. If the charge does not reverse on its own and the merchant does not respond within a reasonable time, escalate to your bank.

How to Request a Refund for Duplicate Charges

Requesting a refund for a billing error is straightforward when you follow a clear process:

- Contact the merchant by phone or email and state clearly that you were charged twice for the same purchase.

- Explain the issue with specifics: provide the transaction date, amount, order number, and your payment method.

- Share your evidence: attach screenshots of both charges and your original receipt.

- Request written confirmation of the refund, including an estimated timeline.

- Track the refund: credit card refunds typically take 5 to 10 business days; bank account refunds may take 3 to 5 business days.

If the merchant agrees but the refund does not appear within the stated timeframe, follow up in writing and save copies of all communication.

What If the Merchant Refuses to Help?

If a merchant denies your refund request, becomes unresponsive, or disputes your claim, you still have multiple escalation options:

- Ask to speak with a supervisor or the billing department manager.

- Send a formal written complaint via email or certified mail, clearly documenting the duplicate charge and your request for a refund.

- File a complaint with the Better Business Bureau (BBB) or leave a documented review on RaiseAComplaint.com — public visibility often motivates businesses to respond.

- Escalate to a bank dispute or credit card chargeback (see the next section).

Keep every communication on record. If you eventually need to pursue a chargeback, this paper trail will support your case significantly.

How to Dispute Duplicate Charges with Your Bank or Credit Card Issuer

If merchant-level resolution fails, the next step is to file a formal billing dispute with your financial institution.

Credit Card Disputes

Credit card issuers like Visa, Mastercard, American Express, and Discover have formal dispute processes. Log into your online account or call the number on the back of your card. Most issuers allow you to dispute a charge directly through the app or website. You will be asked to:

- Describe the nature of the dispute (duplicate or incorrect charge)

- Provide the transaction date and amount

- Upload supporting documentation

Once filed, the card issuer will typically issue a provisional credit within a few days while the investigation is ongoing. The full investigation can take 30 to 90 days.

Debit Card Disputes

Debit card disputes follow a slightly different process and are protected under the Electronic Fund Transfer Act (EFTA). Notify your bank as soon as possible. If you report within 2 business days of discovering the error, your liability is limited to $50. Waiting longer can increase your liability.

Chargeback Process

A chargeback is a formal reversal of a transaction initiated by your bank after a dispute. The bank contacts the merchant's bank, which may result in the funds being returned to your account. Chargebacks are generally reserved for situations where the merchant has refused to resolve the issue directly.

Consumer Rights Regarding Duplicate Charges

Federal law provides meaningful protections for consumers dealing with billing errors.

Fair Credit Billing Act (FCBA)

The FCBA applies to credit card accounts and gives you the right to dispute billing errors — including duplicate charges — within 60 days of the statement on which the error first appeared. Under the FCBA, your card issuer must acknowledge your dispute within 30 days and resolve it within two billing cycles (no more than 90 days).

Electronic Fund Transfer Act (EFTA)

For debit card and bank account disputes, the EFTA governs your rights. Banks are required to investigate disputes within 10 business days and must refund the disputed amount if the error is confirmed.

Who Can Help

The Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB) both provide resources for consumers dealing with billing disputes. The CFPB also accepts formal consumer complaints at consumerfinance.gov, which can prompt businesses to respond. You can also submit complaints to your state attorney general's consumer protection office.

|

Card Network |

Dispute Timeframe |

Key Protection |

|

Visa |

120 days from transaction |

Zero Liability Policy |

|

Mastercard |

120 days from transaction |

Zero Liability Policy |

|

American Express |

60 days from statement |

Dispute Resolution Center |

|

Discover |

60 days from statement |

U.S.-based dispute team |

|

Debit Card (FCBA) |

60 days from statement |

Bank must investigate within 10 days |

Common Mistakes Consumers Make When Dealing With Duplicate Charges

|

Common Mistake |

Why It Hurts You |

|

Waiting too long |

Most banks have a 60-day dispute window. Miss it and your options shrink. |

|

Not saving receipts |

Without proof of the original charge, disputes are harder to win. |

|

Filing incomplete disputes |

Missing info causes delays or automatic denials. |

|

Ignoring small amounts |

Scammers often test with small duplicate charges before larger ones. |

|

Contacting the wrong dept. |

Calling general customer service instead of the billing team wastes time. |

How to Prevent Double Billing in the Future

A few simple habits can dramatically reduce the chances of duplicate charges appearing on your account:

- Set up transaction alerts: Most banks and credit card issuers offer real-time notifications for every charge. Enable these in your banking app.

- Review statements monthly: Do not rely on alerts alone — set aside time each month to go through your full statement line by line.

- Track your subscriptions: Use a spreadsheet or subscription tracking app to monitor all recurring charges and their expected billing dates.

- Keep receipts and order confirmations: Save digital receipts in a dedicated email folder so you can quickly cross-reference charges.

- Limit stored payment methods: The more services that store your card details, the higher the chance of a billing error. Remove payment info from sites you no longer use.

- Review automatic payments: Check automatic payment settings regularly and update them whenever you change your payment method.

How RaiseAComplaint.com Can Help

If you have been charged twice, submitted a refund request, and still are not getting anywhere, RaiseAComplaint.com offers a free platform to document and share your experience publicly.

Consumers use RaiseAComplaint.com to:

- Share detailed accounts of billing errors and unresolved duplicate charges

- Raise concerns that are visible to other consumers and to businesses themselves

- Create a documented public record of disputes that merchants have ignored

- Encourage businesses to respond and resolve issues to protect their reputation

Public documentation of a billing dispute can be surprisingly effective. Many businesses monitor platforms like RaiseAComplaint.com and respond to complaints that are visible to potential customers.

The Bottom Line

Finding duplicate charges on your account is frustrating — but you are not powerless. With the right documentation and a clear process, most billing errors can be resolved without significant hassle.

The most important things to remember: act quickly, save everything, and work your way through the proper channels — merchant first, then your bank or card issuer. Federal law is on your side through the Fair Credit Billing Act and the Electronic Fund Transfer Act, and consumer protection agencies like the CFPB and FTC exist precisely to support situations like this.

Do not wait. The sooner you report a duplicate charge, the more options you have and the faster you will see a resolution. And if a business refuses to take responsibility, remember that you have dispute channels, legal rights, and platforms like RaiseAComplaint.com to make your voice heard.

Frequently Asked Questions About Duplicate Charges

1. What should I do if I was charged twice for the same purchase?

First, verify that both charges are genuine duplicates by checking transaction dates, amounts, and merchant names. Then contact the merchant directly with your evidence and request a refund. If the merchant does not resolve it within a few business days, file a billing dispute with your bank or credit card issuer.

2. How long does a refund for a duplicate charge take?

Refund timelines vary by payment method. Credit card refunds typically take 5 to 10 business days from the date the merchant processes the refund. Bank account (debit card) refunds may arrive within 3 to 5 business days. If your bank issues a provisional credit during a dispute, that credit may appear within 1 to 2 business days.

3. Can I dispute duplicate charges on my credit card?

Yes. Under the Fair Credit Billing Act, you have the right to dispute billing errors — including duplicate charges — within 60 days of the statement date on which the error appeared. Contact your credit card issuer by phone or through your online account. Card networks like Visa, Mastercard, American Express, and Discover each have formal dispute procedures.

4. What is the difference between a duplicate charge and a pending authorization?

A pending authorization is a temporary hold placed on your funds when you make a purchase. It appears on your account while the actual transaction processes, which can take 1 to 3 days. A genuine duplicate charge occurs when two separate transactions post for the same purchase. If in doubt, wait 2 to 3 business days before filing a dispute.

5. Will my bank automatically refund duplicate charges?

Not always automatically, but banks are required to investigate billing disputes and issue refunds if an error is confirmed. For credit cards, the FCBA mandates resolution within two billing cycles. For debit cards, banks must investigate within 10 business days under the EFTA. Filing a formal dispute is usually necessary to trigger the refund process.

6. How long do chargeback investigations take?

Chargeback investigations typically take between 30 and 90 days. Your credit card issuer may issue a provisional credit to your account while the investigation is ongoing. Debit card disputes must be investigated within 10 business days (or 45 days if the bank needs more time, with a provisional credit issued in the interim).

7. Should I contact the merchant before my bank?

Yes, in most cases. Contacting the merchant first gives them the chance to correct the billing mistake quickly. Merchants can often issue a refund faster than a bank dispute can be resolved. It also demonstrates good faith, which strengthens your position if you later need to file a formal chargeback with your financial institution.

8. What evidence should I provide when disputing a duplicate charge?

Provide as much documentation as possible: screenshots of both charges on your statement, original receipts or order confirmations, any communication with the merchant, and the transaction dates and amounts. The more clearly you can show two identical charges for one purchase, the stronger your dispute will be with both the merchant and your bank.

9. What if the duplicate charge is for a subscription?

Contact the subscription company's billing support team first. Provide your account details and evidence of the double charge. Most reputable subscription services will refund a confirmed duplicate payment promptly. If they do not respond or refuse, file a dispute with your credit card issuer and consider canceling the subscription to prevent future issues.

10. Can I report a billing dispute on RaiseAComplaint.com?

Yes. RaiseAComplaint.com is a free U.S.-based consumer platform where you can publicly document unresolved billing disputes, including duplicate charges and double billing issues. Submitting a complaint creates a visible public record that can prompt businesses to respond, and it helps other consumers identify patterns of billing errors with a particular merchant.